The Power of Words: How Current is Your Firm’s Lexicon?

Some chatroom banter that slipped through the net.

The spectre of the LIBOR rigging cartels was raised this quarter when a sweep of e-comms across three big banks revealed the chatter of multiple rogue traders brazenly boasting as they went about manipulating the futures market.

The Commodities Futures Trading Commission orders revealed some surprising chatroom dialogue that had slipped through the net at Deutsche Bank, HSBC and UBS, sending a message to others in the sector that email and other communications surveillance, and acting on what you find, is now mission critical.

With echoes of the incriminating chats that gained global notoriety when it emerged that traders were using exclusive rooms to collude and fix LIBOR, once again those alleged to have manipulated markets gave themselves nicknames as they aligned strategies and shared information.

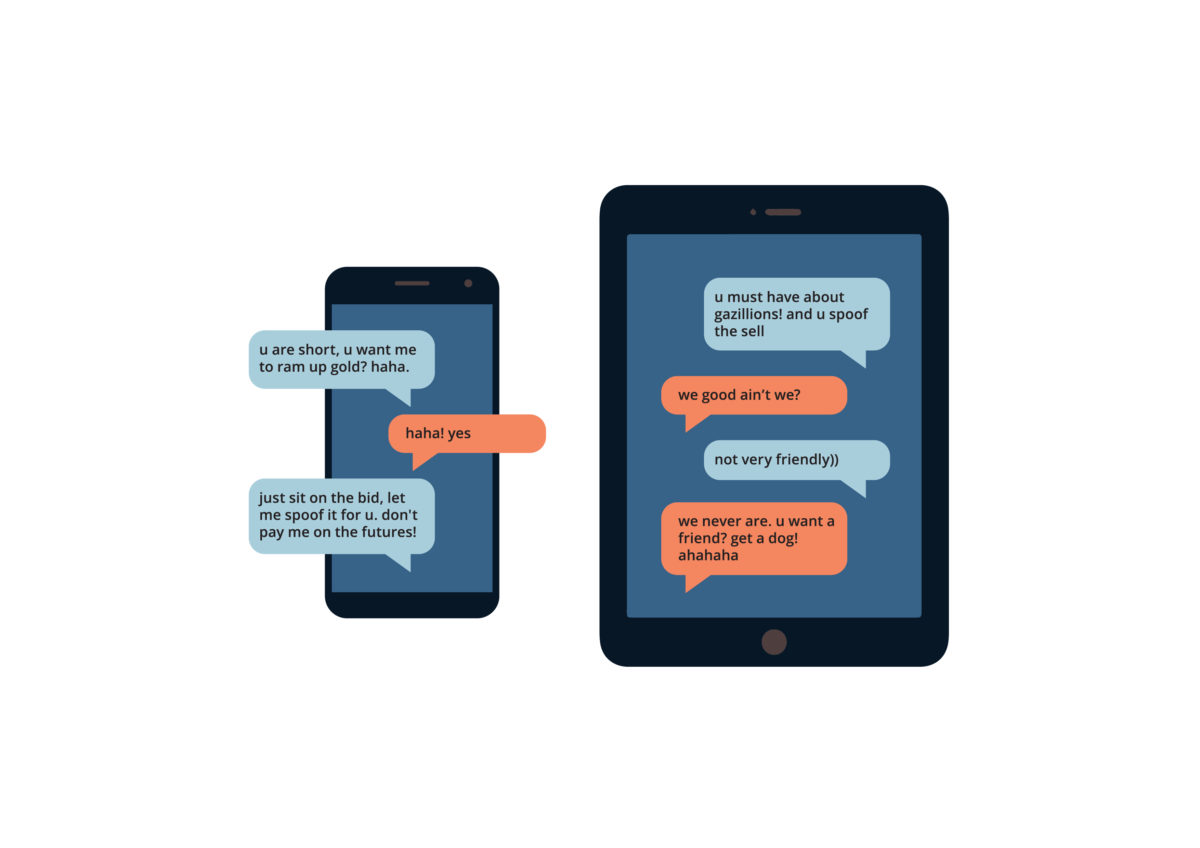

“We good ain[’]t we”, says one UBS trader, who is told they are “not very friendly.”

“we never are … u want a friend … get a dog … ahahahah,” came the response.

A dog may provide company, but it’s not going to guard against the CFTC and US Department of Justice enforcers who have put down a significant marker in the fight against spoofing.

The act involves placing large bids or offers in the futures market with the intent to cancel before execution after another smaller bid or offer is placed on the opposite side of the same market.

The purpose of the scheme is to create the false appearance of market liquidity, which in turn creates the impression of greater buying or selling interest than legitimately exists.

It can be tough to prove, because spoofing is typically a solo act and communication trails are often thin on the ground, or easily attributable to other instances of market activity or just trivial discussions.

Moreover trade data in isolation is not easy to monitor because the placing and cancelling of orders is not immediately indicative of spoofing.

However in this case it was different, replicating the back-and-forth dialogue of the groups who fixed the London Interbank Offered Rate in one of the largest financial scandals ever to be uncovered, the traders freely admitted, and even in some instances trained others, to spoof.

The charges against the top European banks will likely serve as a timely reminder for organizations to invest more time in their e-comms surveillance programs.

Not only by shoring up their lexicon but also by ensuring appropriate escalation levels and processes for investigating and resolving alerts generated by platforms.